- Employee Benefits

- Article

- 6 min. Read

- Last Updated: 06/17/2021

Offering a 401(k)? Know Your Fiduciary Responsibility

Table of Contents

Offering your employees a retirement plan is about more than helping them achieve a comfortable retirement; it's also about following regulations to ensure that your business is protected from liability. Fiduciary responsibility is one concept you'll need to understand before you offer a plan to your employees.

What is a Fiduciary?

According to the Small Business Association, Americans will typically live almost 20 years past what has traditionally been considered retirement age, which, together with the decline of corporate pensions, makes offering a 401(k) plan attractive to employers and employees. By offering your workers the chance to take advantage of compound interest you can help them work toward a more comfortable retirement. But before you offer your employees a retirement plan, it's important to understand the concept of fiduciary responsibility. Let's explore what that means, and how to help ensure that you'll be able to meet your responsibilities.

According to the IRS, a fiduciary is "a person who owes a duty of care and trust to another and must act primarily for the benefit of the other in a particular activity." With regard to retirement plans, the fiduciary is responsible for looking out for your employees’ best interest when it comes to their retirement savings.

Once you offer your employees a retirement plan, you either become the fiduciary or you'll need to hire someone to take over some fiduciary responsibilities.

ERISA and Different Types of Fiduciaries

ERISA stands for the Employee Retirement Income Security Act of 1974. This act is currently the major law governing employee retirement plans, ensuring that both employees and employers are taken care of fairly.

Within ERISA, there are several types of fiduciary roles that make decisions about managing the plan or its investments. Understanding ERISA fiduciary responsibilities will help make a retirement plan safe for your staff.

1. Named Fiduciary

Under ERISA Section 402, each plan must have a named fiduciary who is the "go-to" person with regard to operation and administration of the plan. This person is responsible for choosing and monitoring other plan fiduciaries and service providers. Often, the named fiduciary is the plan sponsor who is typically the employer or owner of the company offering the plan to employees.

2. Trustee

Under ERISA Section 403, unless certain exceptions apply, plan assets must be held in trust, making the role of a trustee necessary. A trustee is the person such as the business owner or group of people who are responsible for managing the assets in the trust, including oversight of contribution processing, investment transactions, financial statements, and fees and expenses.

3. 3(21) Investment Advisor Fiduciary

This fiduciary recommends investments for the plan but does not have discretion to implement those recommendations. The 3(21) fiduciary will also monitor the plan's investments and suggest modifications as needed. The plan sponsor maintains responsibility for the investment decisions.

4. 3(38) Investment Manager Fiduciary

This type of ERISA fiduciary has full discretion to choose, manage, or remove investments within the employee benefit plan.

5. 3(16) Plan Administrator

Plan administrator responsibilities include managing the day-to-day decisions and operation of the plan. Unlike an ERISA 3(21) or 3(38) fiduciary that focuses on the investments in a retirement plan, the role of a 3(16) fiduciary relates to administrative duties. Some 3(16) fiduciary duties may include:

- The monitoring, hiring, and firing of service providers;

- Filing Form 5500;

- Monitoring plan operations;

- Distributing annual notices; and

- Approving distributions and loan requests.

What is Fiduciary Responsibility?

The essential elements of fiduciary responsibility are outlined by the Department of Labor and the IRS:

- Acting in the sole interest of the participants and their beneficiaries

- A written plan that describes the benefit structure and guides day-to-day operations

- A trust to hold the plan's assets

- A recordkeeping system to track the flow of monies going to and from the retirement plan

- Documents to provide plan information to employees participating in the plan and to the government

- Acting for the exclusive purpose of providing benefits to workers participating in the plan and their beneficiaries, and defraying reasonable expenses of the plan

- Carrying out duties with the care, skill, prudence, and diligence of a person familiar with the matters

- Following the plan documents

- Diversifying plan investments

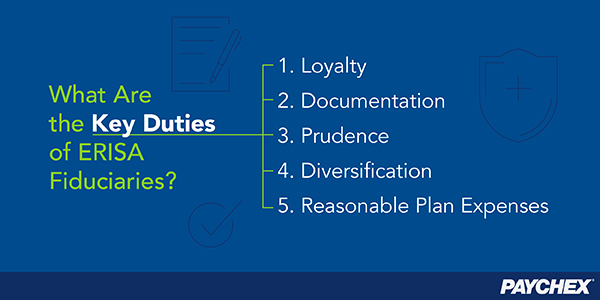

What are Key Duties of ERISA Fiduciaries?

There are several duties required to uphold ERISA standards to ensure the plan is working in the best interests of the employees.

1. Loyalty

Usually loyalty lies on the shoulders of the plan's trustee. Because a trustee is responsible for overseeing money, they must act solely in the best interest of the beneficiary.

2. Documentation

Communication and clear documentation with your service provider and plan provider will help ensure your plan document is written to comply with all requirements in the Internal Revenue Code. This method will also ensure that a plan is carried out in a strategic operational fashion.

3. Prudence

According to ERISA, actions made for a retirement plan must be made with care, prudence, skill, and diligence. To protect employees and their money if a company cannot carry out the fiduciary responsibilities, they must hire someone who has the appropriate skills to carry out these responsibilities.

4. Diversification

Generally, a well-diversified retirement account can provide less risk for plan losses. A fiduciary must assess a particular investment or investment course of action to determine if it is designed to further the purposes of the plan, taking into consideration the risk of loss and the opportunity for gain associated with such investment.

5. Reasonable Plan Expenses

Reviewing your current plan and measuring the costs and expenses against the services provided are an important part of ensuring you're handling your retirement accounts properly.

Your Potential Liability

Fiduciary responsibility also comes with liability. If an organization cannot adhere to the basic rules of fiduciary responsibility, the organization along with the individual fiduciaries can become liable for losses to the plan. Organizations and individual fiduciaries can also be held accountable for any assets gained through improper implementation of the plan. For these reasons it becomes incredibly important to establish a strong plan, meticulously document the process you've established, and continue to check in frequently to ensure the accuracy of your reporting.

Hiring a Service Provider May Be a Great Option

If your company offers a retirement option, you'll need to be aware of your fiduciary responsibilities. But you don't have to handle the process on your own. Do some research and you'll find that some third-party retirement services providers can help alleviate some of the fiduciary responsibilities for you.

When you've outsourced the management of your fiduciary responsibilities or hired internally for the position, you've taken the first step in your process and must abide by certain regulations. A third party can help answer questions and concerns your organization may have while determining the appropriate retirement plan for your employees. Issues you may need to solve include meeting an implementation deadline, or understanding exactly what key plan documents are needed to get the ball rolling.

Setting up a retirement account can be a wonderful option for your employees who are interested in participating. Setting up and managing a 401(k) plan doesn't have to be complicated and you don't have to do it alone. With assistance from the right 401k service provider, you can find your business right on track to meet its fiduciary responsibilities.

Tags