State Mandated Retirement Programs — Are You Ready?

Many states now require employee retirement savings options. A Paychex 401(k) plan offers advantages over state IRAs:

- Potential tax credits up to $16,500 for small businesses¹

- Additional annual credits with employer contributions¹

- Greater flexibility and control

What’s Happening in Your State?

State retirement rules aren't one-size-fits-all. Do you have employees in different states? You could be juggling multiple sets of requirements.

Click on any state to see what you're dealing with.

New York

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Ohio

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

North Dakota

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

North Carolina

Program Status

Iowa

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

New Jersey

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

New Hampshire

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

District Of Columbia

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

California

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Nebraska

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Indiana

Program Status

Wyoming

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Wisconsin

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Illinois

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

West Virginia

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Nevada

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

State Website

Idaho

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Maryland

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Maine

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Washington

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More

New Mexico

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

State Website

Louisiana

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Utah

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Hawaii

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Texas

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Virginia

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Vermont

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

State Website

South Carolina

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Rhode Island

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

State Website

Kentucky

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Kansas

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Florida

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Georgia

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Pennsylvania

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Oregon

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Oklahoma

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Montana

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Delaware

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

State Website

Connecticut

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Colorado

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Learn More About The State Mandate

State Website

Arkansas

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Arizona

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Tennessee

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Missouri

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

South Dakota

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Mississippi

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Alaska

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Alabama

Program Status

No Recent Legislation

At this time, does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Minnesota

Program Status

Employer Participation

Program Type

Employer Qualifications

Program Details

Penalty

Program Website

Michigan

Program Status

Massachusetts

Program Status

Employer Participation

Program Type

Employer Qualifications

State Website

STATE

Program Status

No Recent Legislation

At this time, STATE does not have any recent legislation related to state-facilitated retirement programs. We will continue to monitor the situation. Please check back with Paychex regularly for updates.

Paychex 401(k): Comprehensive Benefits That State Plans Simply Can't Match

Meet State Mandates With Ease

Paychex 401(k) plans:

- Fully satisfies state retirement plan requirements

- Includes expert help with setup and ongoing administration

Help Employees Save More, Faster

401(k) plans from Paychex:

- Offer over 3x the contribution limit of IRAs, meaning employees can potentially build retirement savings faster and more effectively

Maximize Tax Credits

Paychex 401(k) plans are:

- Eligible for SECURE Act tax credits—up to $16,5001

- Potentially eligible for an additional $1,000/year in credits with employer contributions1

Simple Payroll Integration

Choose Paychex 401(k) and:

- Seamlessly integrate with Paychex payroll—one platform, one provider

- Get support from a leading 401(k) provider in the nation2

State IRA or 401(k) Plan — Which Is Better for Your Business?

IRA vs. Paychex 401(k) Plan

State - IRA

401(k) Plan (Offered with Paychex)

$7,500

$24,500

No

Yes, at employer's discretion

Not available

Potential tax credits of up to $5,500 per year for the first 3 years.

Potential employer contribution credit of $1,000 (maximum) per employee 2

Employer processes payroll contributions, updates contribution rates, adds newly eligible, etc.

Paychex makes administration simpler as your recordkeeper

Getting Started With Paychex 401(k) Is Simple

Get in Touch

Fill out our form to speak with a retirement plan specialist who can answer your questions.

We’ll Help You Find the Right Plan

Do you want full control or prefer we handle everything? We'll help you choose the right level of service for your business.

We’ll Help You Get Set Up

We'll guide you through setup and employee enrollment so you can launch your plan with confidence.

Complete 401(k) Solutions: From Setup to Management

Our platform makes everything easier—from signing up employees to managing accounts and staying compliant.

-

Easy Account Access

Easy Account Access

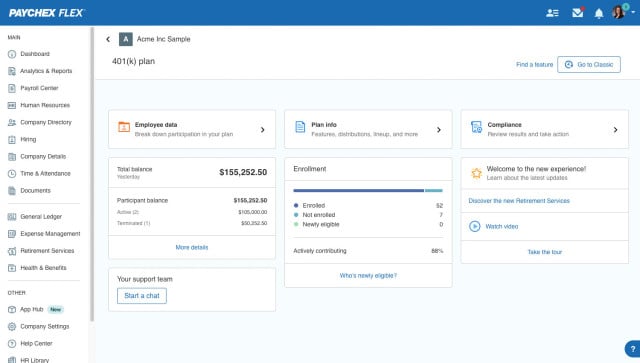

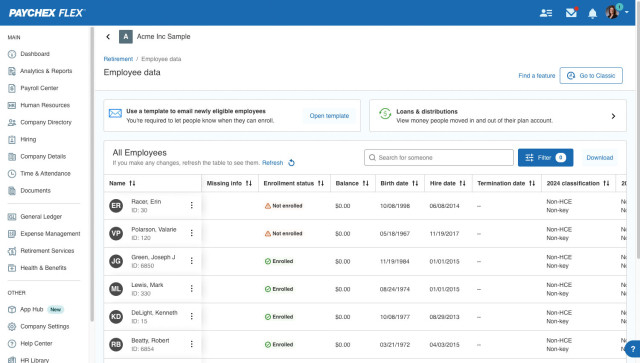

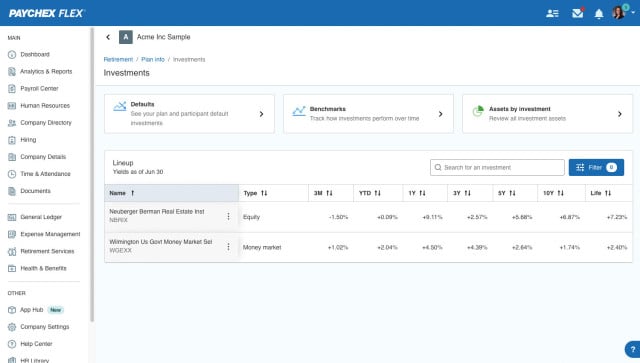

Easily manage accounts, check retirement contribution amounts, maximize 401(k) contributions, review investment performance, and more from the account dashboard.

-

Sign Up in 4 Clicks

Sign Up in 4 Clicks

The quick enrollment feature allows employees to sign up for a retirement plan in four clicks. When you integrate payroll, you can easily see who is eligible for your chosen retirement plan.

-

Let Us Do the Heavy Lifting

Let Us Do the Heavy Lifting

Simplify processes like 401(k) investment selection, changing plan contributions, and checking the status of a loan. For even more convenience, our Pooled Employer 401(k) Plan offers simplified administration and enrollment, reduced fiduciary liability, and savings potential.

-

Compliance Support

Compliance Support

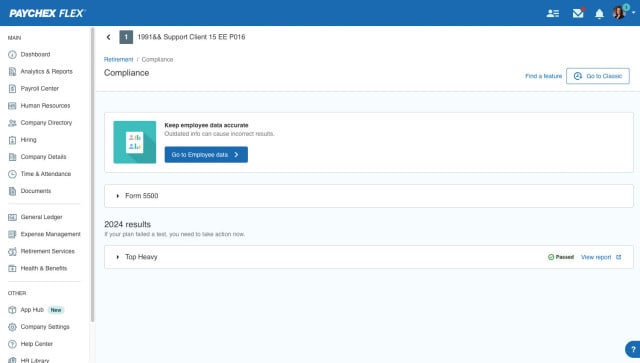

As part of our retirement services, our Paychex Flex® platform can improve reporting accuracy, collect important data, and our retirement specialists are available when you need them for expert advice and compliance assistance.

The Importance of Offering a Retirement Plan

A large percentage of Americans are not building up sufficient assets needed to maintain their standard of living in retirement, and the problem is only getting worse for younger generations.

80%

of all workers feel people in their generation will have a much harder time achieving financial security.3

60%

of workers concerned about governmental changes are worried about their Social Security benefits being reduced.4

1/4

25% of civilian and 28% of private industry workers in the U.S. do not have access to a retirement savings plan.5

69%

of workers believe they could work until retirement and still not save enough to meet their needs 3

How a California Business Made Retirement a Fixture

With the state of California requiring most employers to offer an employee retirement option, Plumbing M.D. embraced the opportunity and turned to Paychex.

The business saw some surprising results: 100 percent participation in their Paychex 401(k) plan, and employees under the age of 30 who are enthusiastic about the plan.

Unlock More Value with Additional Paychex Services

Experience the strength of Paychex through seamless, integrated solutions on our all-in-one platform.

Retirement Insights

Recognized for Innovation, Ethics, and Performance

State Retirement Plan FAQs

-

What Is State-Mandated Retirement Savings for Businesses?

What Is State-Mandated Retirement Savings for Businesses?

State-mandated retirement savings is a requirement in many states where businesses must either offer their own employee retirement plan or enroll in the state's retirement savings program. If businesses fail to comply with state requirements, they may face penalties. The specific rules, deadlines, and penalties vary by state and business size.

-

Which States Have Mandatory Retirement Plans?

Which States Have Mandatory Retirement Plans?

Multiple states have already launched active mandatory retirement savings programs, including early adopters like Oregon, Illinois, and California. Many additional states have enacted legislation with programs in various stages of implementation, while others are actively considering similar requirements.

The landscape of state-mandated retirement programs continues to evolve rapidly, with new states regularly:

- Enacting mandatory retirement plan legislation

- Launching operational programs

- Updating existing program requirements

- Modifying compliance deadlines and penalties

Due to the rapidly changing nature of state-mandated retirement legislation, employers and benefits professionals should regularly check current requirements for their specific states. Program details, compliance deadlines, and eligibility requirements are subject to change as states refine their programs and new states enact similar legislation.

For the most current information on specific state requirements, penalties, and implementation timelines, refer to our interactive state map and subscribe to receive updates for your state's mandatory retirement program developments.

Impact on Employers

Employers in states with mandatory retirement programs must either:

- Offer a qualified retirement plan (like a 401(k)), or

- Participate in the state-facilitated program, or

- Meet specific exemption criteria, which vary by state

Non-compliance penalties vary by state but can include fines and administrative costs.

-

Is There a Difference Between a State IRA Program and a Traditional 401(k)?

Is There a Difference Between a State IRA Program and a Traditional 401(k)?

State IRAs limit contributions in 2026 to $7,500 annually with no employer matching. By contrast, 401(k) plans allow up to $24,500 in employee contributions plus employer matching that can double retirement savings. Paychex 401(k) plans may offer additional investment options and tax savings.

-

Why Do States Require Employers To Offer Workplace Retirement Savings Programs?

Why Do States Require Employers To Offer Workplace Retirement Savings Programs?

States require employers to offer retirement savings programs because of a national retirement savings crisis. According to the U.S. Bureau of Labor Statistics, approximately 25% of civilian workers do not have access to retirement savings.4 To address this problem, many states and cities have passed laws requiring employers to help employees save for retirement through workplace retirement programs.

-

What Type of Retirement Programs Do States Offer Employers?

What Type of Retirement Programs Do States Offer Employers?

Most states offer Roth Individual Retirement Accounts (IRAs) for their mandatory retirement programs. These state-sponsored Roth IRAs typically:

- Automatically enroll employees at 3-5% of their payroll wages

- Allow employees to opt out or change their contribution amount

- Require some administrative work from employers

- Feature state-selected investment options chosen by the state's program board

-

Does My Business Have To Participate in a State-Facilitated Retirement Savings Program?

Does My Business Have To Participate in a State-Facilitated Retirement Savings Program?

No, you don't have to participate in your state's retirement program. Instead, you can offer your own private retirement plan, such as a 401(k), to meet your state's requirements. This allows you to maintain control over your employee benefits while still complying with state mandates.

-

Why Should I Consider a Private-Sector 401(k) Plan Versus a State IRA?

Why Should I Consider a Private-Sector 401(k) Plan Versus a State IRA?

A 401(k) plan offers several advantages over state IRA programs:

- Higher contribution limits: Employees can save significantly more money faster with a 401(k)

- Tax credits: New 401(k) plans may qualify for SECURE Act tax credits (not available with state IRAs)

- Reduced administrative burden: Options like Pooled Employer Plans (PEPs) minimize time and management costs.

- Employee attraction: 401(k) plans are popular with employees and help with recruiting

- Flexibility: Choose a plan that fits your business needs and employee savings goals

The best choice depends on your specific business requirements and what your employees need for retirement savings.

-

What Are the Penalties for Not Complying With State Requirements?

What Are the Penalties for Not Complying With State Requirements?

Penalties for not complying with state retirement savings laws vary by state and can be expensive. For example:

- California (CalSavers): $250 per eligible employee after 90 days of non-compliance, increasing to $500 per employee after 180 days

- Penalties multiply quickly: Even small businesses with only a few employees can face significant fines

- Ongoing costs: Penalties typically continue until you comply with state requirements

The specific penalty amounts and timelines differ by state, so it's important to understand your state's requirements and deadlines to avoid costly fines.

-

What if I Already Offer an Employee Retirement Plan?

What if I Already Offer an Employee Retirement Plan?

If you already offer an employee retirement plan, you can typically register for an exemption from your state's retirement program. This means you won't have to participate in the state IRA program as long as you maintain your existing retirement benefits.

To get an exemption:

- Contact your state's retirement program office

- Follow your state's exemption registration process

- Provide documentation of your existing retirement plan

Check your state's specific requirements and deadlines to ensure you properly register your exemption and avoid penalties.

-

How Do I Stay Up to Date on My State’s Retirement Mandate Laws?

How Do I Stay Up to Date on My State’s Retirement Mandate Laws?

State retirement mandate laws are constantly changing, with many are still being proposed or implemented. To stay current:

- Check your state's official retirement program website regularly for updates

- Monitor implementation timelines: Many laws have delayed or phased rollouts

- Review compliance deadlines: Requirements often vary by business size and industry

- Consult with benefits professionals who track state-by-state changes

Since these laws are evolving rapidly, it's important to stay informed about your state's requirements, deadlines, and any changes that might affect your business.