Flexible Spending Account (FSA) Benefits from Paychex

Boost your health benefits and save on costs with a Paychex Flexible Spending Account (FSA). This pre-tax plan helps employers cover medical and dependent care expenses, lowering taxes and increasing take-home pay.

The Benefits of Offering an FSA

Key Benefits for Employers

- Tax Savings: Lower your FICA taxes with employee FSA contributions (excluding PEO Sponsored FSAs)

- Boost Loyalty: FSAs cover gaps in insurance, keeping employees happy and committed

- Minimal Expense: FSAs require relatively minimal expenses for the business and offer control over plan details such as the carryover or grace period options, or neither.

Key Benefits for Employees

- Save on Taxes: Contribute up to $3,400 in 2026 for eligible medical expenses

- Boost Take-Home Pay: Lower taxes = more money in your pocket

- Instant Access: Full annual funds on your FSA debit card right away

- No Payback: Leave mid-year? You don’t owe a thing

- Manage with Ease: Track funds online anytime

- Carry Over: Rollover unused funds into next year (limited by plan document)

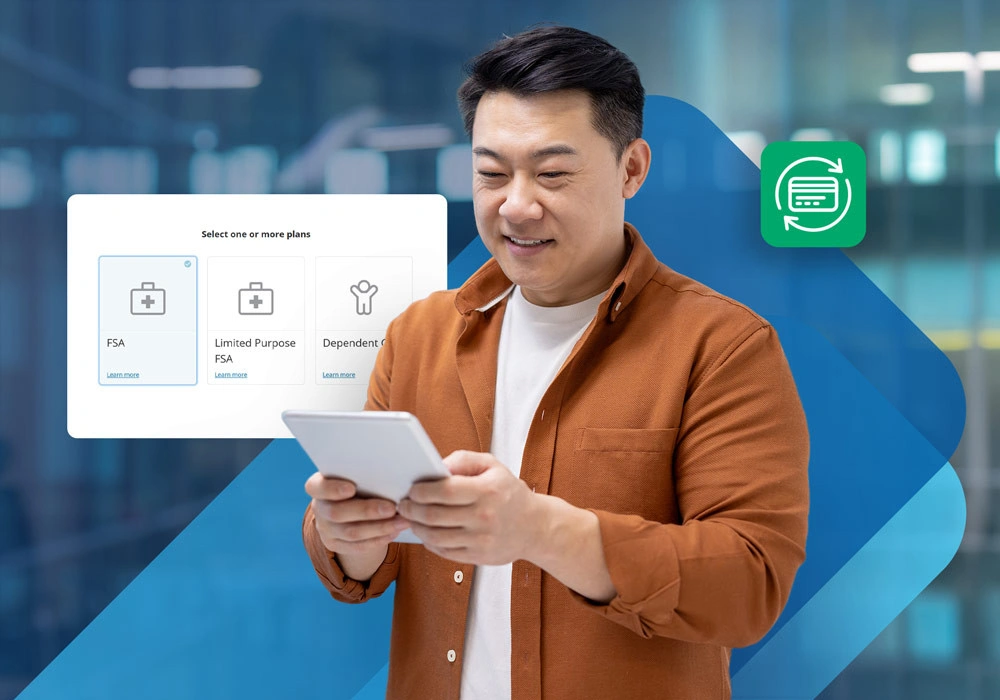

Choose the Type That Works for You

Paychex FSAs: Flexible, customizable, and designed to help you save.

Health Care FSA

Also known as a medical FSA, this lets employees use pretax funds for out-of-pocket eligible medical expenses like co-pays and deductibles. Funds are available upon enrollment and are deducted from payroll.

Transportation FSA

Employees can deduct up to $340/month pretax for commuting, parking, and transit expenses in 2026 and get reimbursed for eligible costs.

Dependent Care FSA

A dependent care FSA lets employees use pretax funds for eligible expenses like daycare or summer camp. Funds become available after each contribution, and costs are reimbursed after being paid for.

Limited Purpose FSA

A limited purpose FSA works alongside an high-deductible health plan (HDHP) and HSA to cover eligible dental and vision expenses. Funds are available on the first day of the plan year.

Flexible Benefits, Your Way

Choose standalone FSAs or combine them with HSAs and HRAs. We'll help you build a package that fits your needs and works seamlessly with your existing setup.

Want to explore all your options? Check out our packages:

How To Get Started With Paychex FSA

Activate FSA Benefits

Work with your Paychex representative to enable FSA management on Paychex Flex®.

Streamline Payroll Deductions

Set up pre-tax payroll deductions and optional employer matching.

Make Enrollment Easy

Help employees enroll and maximize their FSA funds with ease.

Strengthen Your FSA Program With Other Integrated Solutions

Estimate Your Healthcare Savings and Tax Benefits

Discover how much you can save on healthcare and maximize your tax benefits with our easy-to-use calculator.

Recommended for You

FSA Frequently Asked Questions

-

What Is Covered Under an FSA?

What Is Covered Under an FSA?

Employees can choose how much to contribute to their healthcare flexible spending accounts. These contributions are typically used to reimburse eligible expenses like co-payments, out-of-pocket medical costs, and certain dental expenses such as non-cosmetic orthodontics and extractions. Check out our article on what is eligible for FSA reimbursement or the FSA Store for a comprehensive list.

Quick reference tools such as a one-pager or web page can lighten the load for HR professionals by listing common Health FSA-eligible items, including:

- Dentures

- Eyeglasses/contact lenses

- Laser eye surgery

- Medical monitoring devices

- Walking assistance devices

- Wheelchairs and repairs

- Sterilization

Apart from Medicare premiums, FSAs cover many of the same qualified medical and dental expenses as an HSA. Review IRS Publication 502 for details or refer to our article on the differences between FSAs and HSAs here.

-

How Do Employees Use Their FSA?

How Do Employees Use Their FSA?

FSA participants can pay for eligible items or services with an FSA debit card or get reimbursed by submitting proof of expenses.

-

What Are Some Ineligible FSA Items?

What Are Some Ineligible FSA Items?

Participants cannot use their FSA accounts for some items, such as:

- Cosmetic surgeries provided for reasons other than correcting congenital deformities, disease disfigurement, or to correct personal injuries that result from accidents or trauma

- Childbirth class expenses for the coach (those for the expectant mother are covered)

- Exercise equipment for general wellbeing

- Marriage counseling

This is not comprehensive list, so be sure to check which items are eligible.

-

Do FSAs Cover Employees’ Over-the-Counter Medication?

Do FSAs Cover Employees’ Over-the-Counter Medication?

Health care FSAs cover over-the-counter drugs and remedies. Some examples of FSA-eligible items include:

- Indigestion medications

- Eye drops

- Laxatives

- Pain relievers

- Sleep aids

- Acne medications

- Diaper rash ointment

- Ointments for minor injuries

-

What Should Employers Consider When Choosing an FSA Plan?

What Should Employers Consider When Choosing an FSA Plan?

If you wish to offer employees an FSA account plan, the timing of your decision is imperative. Ideally, your new FSA should be ready to go before the following year's open enrollment. This will allow employees to do their research and make their plan elections accordingly. If you currently offer an FSA and need to amend your plan, be sure to communicate any changes to participants.

-

What Is the FSA Carryover or Grace Period Option?

What Is the FSA Carryover or Grace Period Option?

Although not required, employers have two options they can institute to help employees take advantage of all the money they’ve contributed to their healthcare or limited purpose FSAs.

- Allow employees to carry over up to $680 of unused health FSA money in 2026 at the end of the year to apply to the next plan year (remaining funds in excess of $680 are still forfeited to the plan); or

- Elect a grace period to permit employees to use their unused account balances to pay for medical costs incurred during the first 2.5 months of the following plan year (up to March 15 for calendar year plans) before they must forfeit the money.

Before making a final decision, employers should carefully weigh health care or limited purpose FSA benefits or any insurance benefit account and understand the administrative requirements of a carryover or grace period option.

-

When Do You Need To Pick the Carryover or Grace Period Option?

When Do You Need To Pick the Carryover or Grace Period Option?

Both options are intended to reduce “wasteful” end-of-year spending as employees hurry to spend their health care or limited purpose FSA accounts rather than lose the money. Employers are not required to offer either option, in which case the “use it or lose it” rule will still apply. But if you offer one of these options to your workforce, you must pick only one, as employers cannot allow employees both a carryover and a grace period for the health or limited purpose FSA.

You may wish to review any available data on current FSA utilization before deciding which option would work best for your company’s workforce. Once you make your selection, notify employees as soon as possible to give them enough time to make an account selection and adjust their medical spending as needed.

-

How Do You Educate Employees About Flexible Spending Accounts?

How Do You Educate Employees About Flexible Spending Accounts?

Communication efforts about an FSA should be easy to understand and designed to educate employees on the advantages of this benefit account. An FSA quick reference guide listing common items employees can use their FSA funds to pay for is also helpful. You can also provide commonly asked questions, key enrollment dates, and examples that break down different cost scenarios. You'll also want to remind employees about any FSA spending deadlines and clearly explain the carryover or grace period options made available to them, including specific dates and deadlines.

-

How Do You Set Up an FSA?

How Do You Set Up an FSA?

If you're not currently offering an FSA, this can bring tax savings for both you and your employees and provide a much-desired add-on to your health benefits. Paychex offers assistance with FSA implementation, ongoing administration, and the development of employee communications to encourage participation.

-

How Can Employers Stay Compliant With FSA Rules?

How Can Employers Stay Compliant With FSA Rules?

To create a robust employee benefits strategy and maintain compliance, it is imperative to factor in flexible spending account employer rules. To start, employers should understand IRS guidelines and create a clear plan that outlines the terms, eligibility criteria, and limitations of their FSA accounts. Communicate aspects such as eligible expenses and FSA employer contribution limits to employees so everyone is on the same page. Also, file the required forms, perform periodic audits, and confirm dependent eligibility when necessary.

-

Can Small Businesses Offer FSAs?

Can Small Businesses Offer FSAs?

Yes, an FSA for small business owners is possible. Consider if the benefits of an FSA account align with your priorities and are something you want to offer employees. If these things align, a benefits broker or an FSA provider for small businesses can help you provide this to employees, allowing them access to affordable healthcare and tax savings.